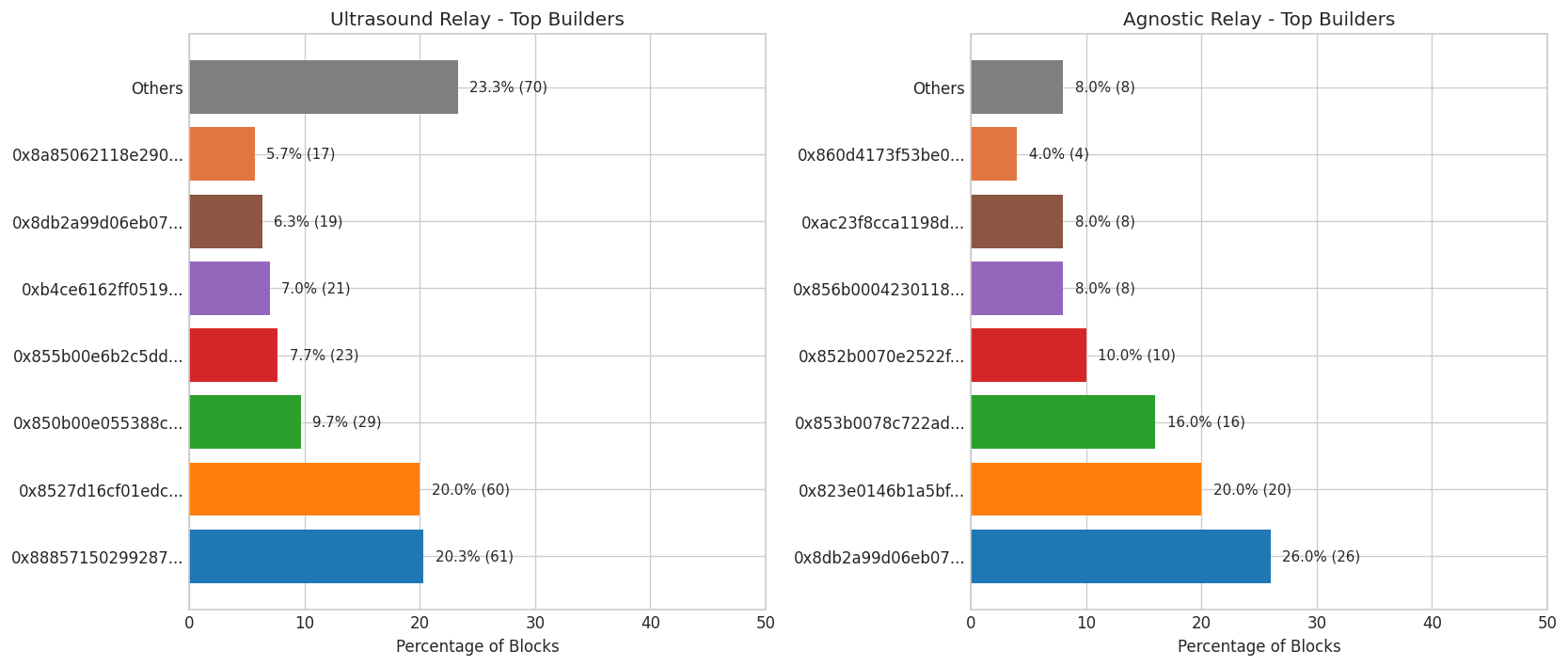

I pulled data from two major MEV relays and found the same pattern on both: a small group of builders dominates. On Ultra Sound, the top builder wins nearly 20% of slots. On Agnostic, it's 26%. Combine the top 3 on either relay and you're looking at roughly half the blocks.

That concentration could mean different things. Maybe a few builders have genuinely better algorithms. Maybe there are economies of scale in MEV extraction that naturally favor incumbents. Or maybe the barriers to entry are just higher than we'd like.

Here's what surprised me: Ultra Sound and Agnostic serve the same Ethereum network, same slots, same validators—but they're completely different markets.

| Metric | Ultra Sound | Agnostic |

|---|---|---|

| Blocks analyzed | 300 | 100 |

| Unique builders | 28 | 13 |

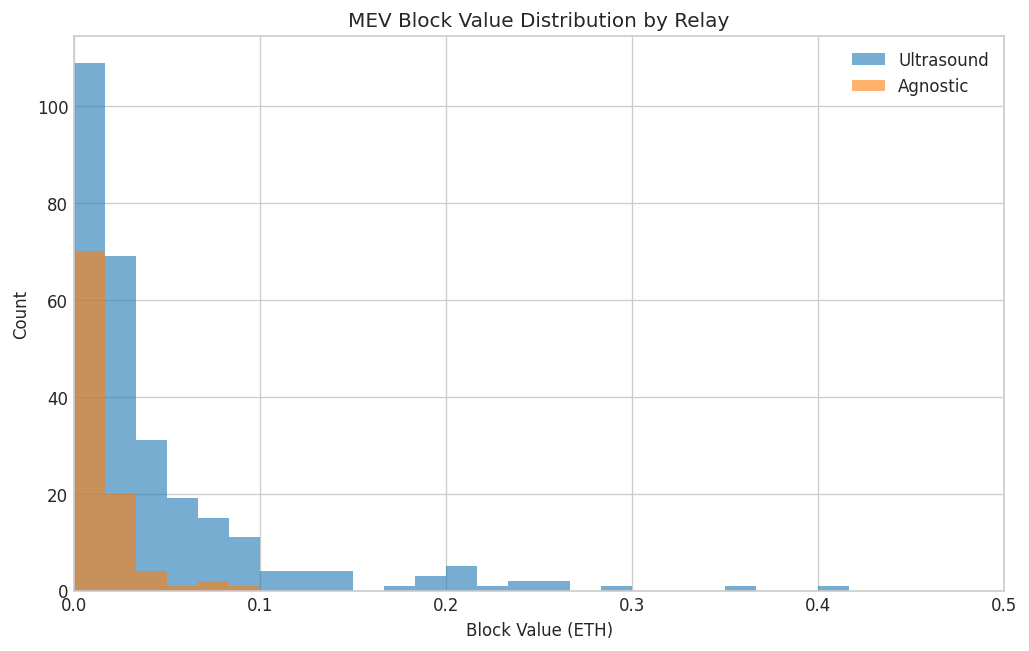

| Average block value | 0.1208 ETH | 0.0378 ETH |

| Median block value | 0.0267 ETH | 0.0120 ETH |

| Max block value | 4.4851 ETH | 1.3618 ETH |

Ultra Sound has more than twice as many builders and delivers blocks worth 3x more on average. The big MEV opportunities clearly flow toward Ultra Sound. Whether that's because sophisticated builders self-select there, or because Ultra Sound has better latency/connectivity creating a virtuous cycle, I can't say from this data.

Look at the gap between average and median values. On Ultra Sound, the average is 0.12 ETH but the median is only 0.027 ETH. On Agnostic, 0.038 ETH average vs 0.012 ETH median.

This is a classic heavy-tailed distribution. Most blocks are routine—small arbitrages, a few priority fee transactions. Then once in a while, someone sandwiches a whale trade or catches a big liquidation, and suddenly you're looking at 4+ ETH block values.

The "average MEV block" doesn't really exist as a typical experience. You're either grinding small opportunities or occasionally hitting the jackpot.

Source: Relay APIs

relay-analytics.ultrasound.moneyagnostic-relay.netEndpoint: /relay/v1/data/bidtraces/proposer_payload_delivered

Slot range: 13596121 - 13597253 (approximately 24 hours)

# Fetch deliveries with pagination by slot cursor

GET /relay/v1/data/bidtraces/proposer_payload_delivered?limit=100

# Use min(slot) from previous batch as cursor for next batchI'm genuinely unsure whether this concentration is a problem.

On one hand, specialized builders efficiently extracting MEV feels different from validator centralization. The builders are competing to deliver value to validators, and validators are free to switch relays or build locally. The market is working, sort of.

On the other hand, 13 builders on Agnostic? That's not a competitive market, that's a dinner party. If entry barriers are that high, we're depending on a small group's continued goodwill and competence. That makes me nervous.

I'd like to see this same analysis over a longer time period. Is concentration increasing? Are new builders entering and gaining share, or is the incumbent advantage compounding? Those trends matter more than any single snapshot.